Italy's Real Role in Olive Oil (It's Not What You Think)

Ask most people about Italian olive oil and they picture sun-drenched Tuscan groves, artisanal producers hand-picking olives at dawn, and bottles of premium EVOO lining the shelves of every supermarket in Europe. The reality is far more interesting — and far more strategic.

Italy produces roughly 300,000 tonnes of olive oil per year. It exports over 344,000 tonnes. Read that again. Italy exports more olive oil than it produces. The country imports enormous volumes of bulk oil from Spain, Tunisia, Greece, and elsewhere, then blends, bottles, and re-exports it under Italian brands worth €3.09 billion annually. Italy isn't just a producer — it's the world's most sophisticated olive oil trading hub, built on centuries of expertise in selection, blending, and marketing.

For anyone involved in olive oil trade — whether you're an importer sourcing European EVOO, a trader tracking Mediterranean price dynamics, or a producer wondering where your oil actually ends up — understanding how Italy really works is essential.

Production: A Recovery, But Not a Comeback

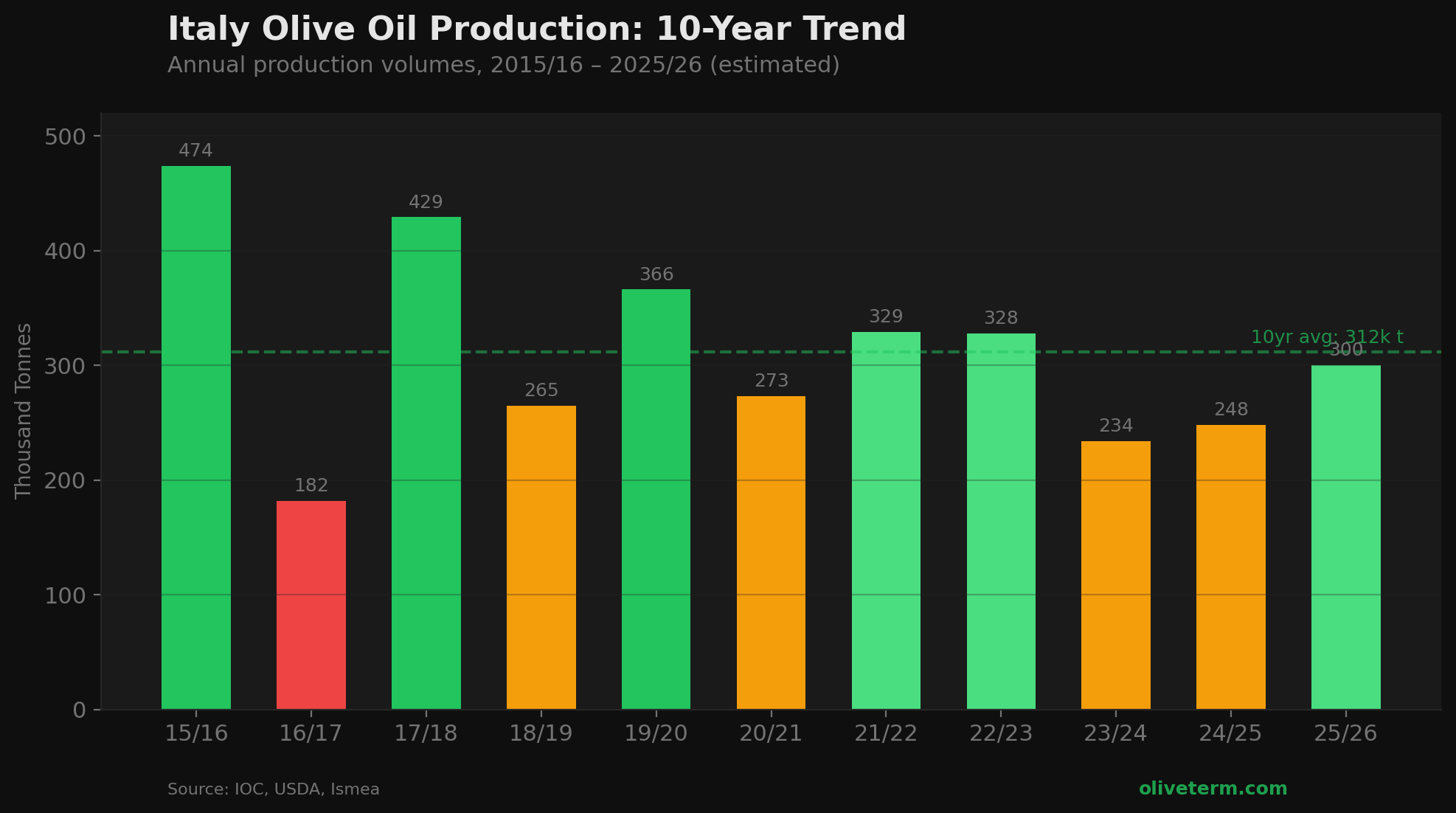

The 2025/26 campaign brought welcome relief. Italian production is estimated at approximately 300,000 tonnes, a 30% bounce from last season's painful 248,000 tonnes. Southern regions drove the recovery, with timely summer rainfall offsetting earlier drought effects.

But let's keep perspective. This is still below the 328,000 tonnes of 2022/23, and nowhere near the 474,000 tonnes Italy managed a decade ago. The long-term trajectory is clear and sobering: aging groves, rising costs, climate volatility, and the ongoing devastation of Xylella fastidiosa in Puglia are structurally eroding Italy's production base.

Where the Oil Actually Comes From

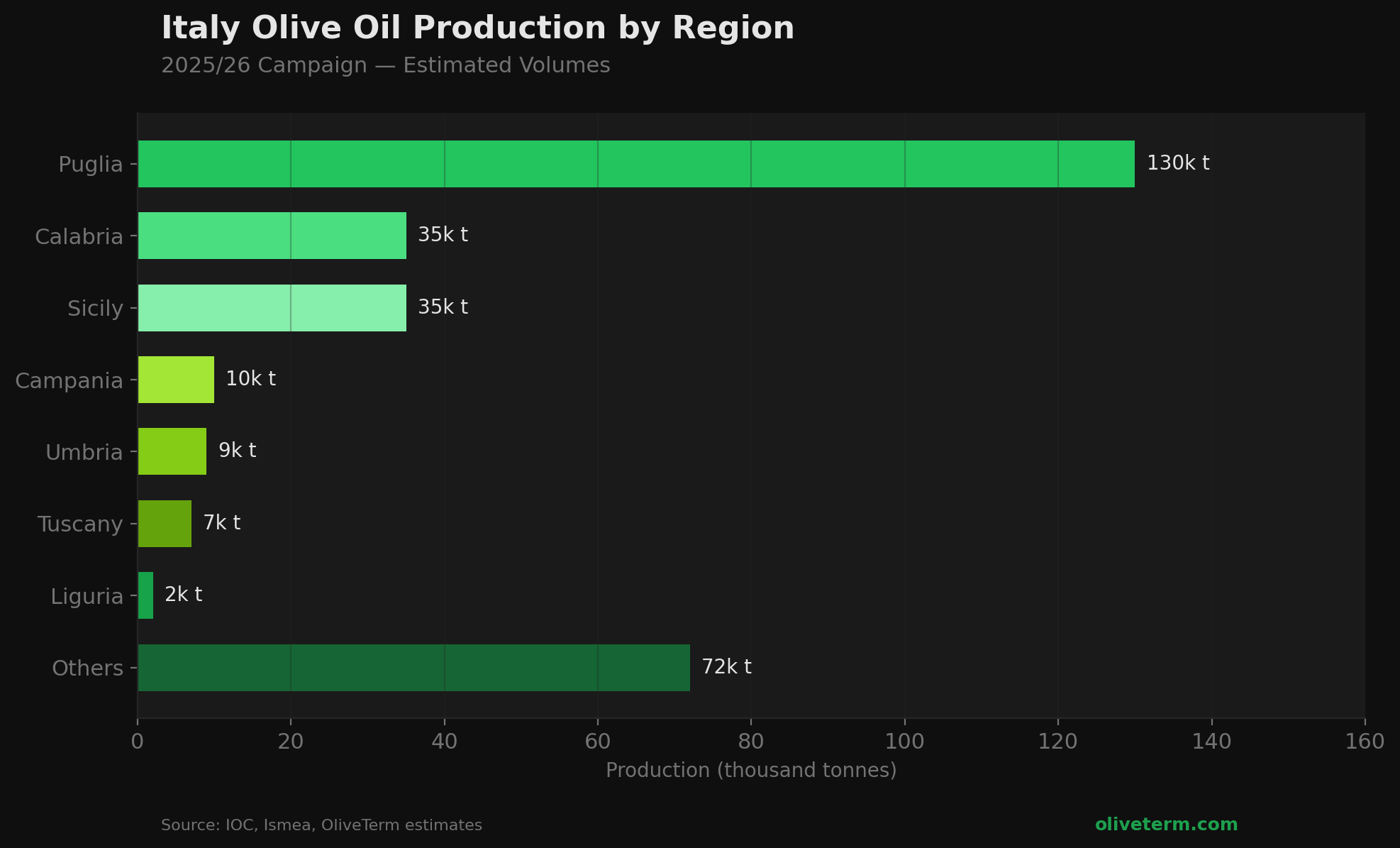

Italian olive oil production is overwhelmingly a southern story:

Puglia is the engine — roughly 40–50% of national output, around 130,000 tonnes this season. It's also where the drama is. Mill-gate prices collapsed from €9.30/kg to €7.40/kg in just three weeks as new-crop volumes flooded the market. For producers who'd spent two years getting used to record prices, the correction was brutal.

Calabria was the quiet winner of 2025/26: over 35,000 tonnes, up 36% year-on-year. Healthy groves, good moisture, minimal pests. If you're sourcing Italian bulk at competitive prices, Calabria is increasingly where to look.

Sicily matched Calabria at roughly 35,000 tonnes, benefiting from well-distributed rainfall and low parasite pressure.

Umbria turned in a solid 8,000–10,000 tonnes of the fruity, slightly bitter oils the region is known for. Tuscany was modest but high-quality, especially from early-harvested Frantoio and Moraiolo. Liguria produced barely 2,000 tonnes — many groves are in alternate-bearing rest, and the famous Taggiasca oils remain rare and expensive.

Campania managed approximately 10,000 tonnes, slightly down, with fruit fly pressure requiring careful monitoring.

The takeaway: Italy's production is increasingly concentrated in a few southern regions, making it vulnerable to localized weather events and pest outbreaks. A bad year in Puglia alone can swing national production by 30%.

Prices: The Hangover After the Party

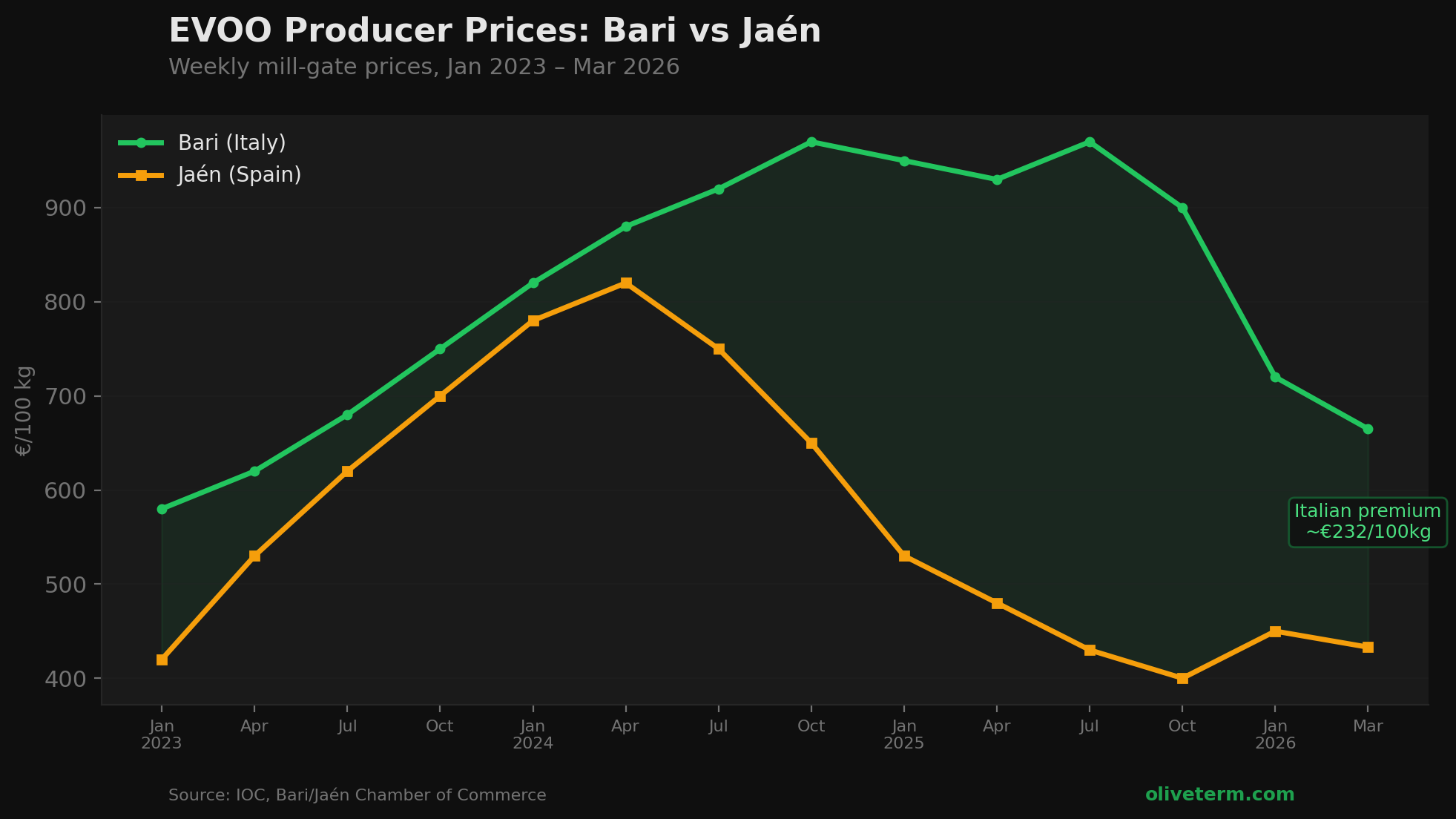

If 2023 and 2024 were the years of record olive oil prices, 2025/26 is the morning after.

EVOO producer prices at Bari — Italy's key benchmark — sit at approximately €6.65/kg as of early 2026, down 30% from the peaks. For context, Bari EVOO touched €9.70/kg in mid-2025 when last season's scarcity was still biting.

The correction makes sense: Spain's 1.37 million-tonne harvest and Tunisia's strong crop have pushed global supply back toward balance. But Italian EVOO still trades at a massive premium over Spanish origin — Jaén is at €4.30–4.50/kg, meaning Italian oil costs roughly 50% more than its Spanish equivalent. That premium reflects brand value and quality reputation, but it also makes Italian origin increasingly expensive for private label and blending.

The DOP and IGP segment tells a brighter story. The 2025 Ismea-Qualivita report showed Terra di Bari DOP and Sicilia IGP production hitting 16,190 tonnes — up 31% from 2023. But here's the uncomfortable truth: certified oils still represent only 6.5% of total Italian EVOO. There's enormous untapped potential in protected designations, and it's arguably where Italy's future competitive advantage lies — not in volume, but in provenance and traceability.

The Hub Machine: How Italy Really Works

This is where it gets fascinating. Italy's trade numbers reveal a business model that most consumers — and even some industry participants — don't fully understand.

The Export Paradox

In 2024, Italy exported 344,000 tonnes of olive oil worth €3.09 billion — a 42.6% increase in value year-on-year. That makes Italy the world's second-largest exporter after Spain, with roughly 20% of the global market.

The catch: those exports exceed national production by nearly 40%. The math only works because Italy imports vast quantities of bulk oil, processes and blends it, then ships it out under Italian labels. It's perfectly legal, often produces excellent blends, and it's what makes Italy the undisputed value-added hub of the global olive oil supply chain.

The key destinations tell the story of where value lies: the United States (highest-value market), Germany (over €268M in imports from Italy), Japan, Canada, and increasingly China (+86.2% growth) and Australia (+60.6%). Italy ships predominantly in containers under 18kg — meaning bottled, branded product, not bulk. That's the premium.

The Import Side

To feed the machine, Italy sources bulk oil from across the Mediterranean. And the flows are shifting fast.

Tunisia now dominates, accounting for 76% of Italy's extra-EU olive oil imports in late 2025. Tunisian imports surged 79.2% year-on-year, driven by competitive pricing — conventional Tunisian EVOO at ~€3.40/kg versus Italian origin at €6.50+/kg. That's roughly half the price. The EU's duty-free quota for Tunisian oil (56,700 tonnes) has been fully saturated for nine consecutive years, and Tunisia is pushing for 100,000 tonnes. If that happens, it would reshape Italy's blending economics significantly.

Argentina, Morocco, and Turkey supply smaller volumes, but the trend is clear: Italy's hub model depends increasingly on non-EU oil, and the regulatory and political dynamics around those flows are becoming more complex.

The Headwinds That Won't Go Away

Xylella: The Slow Catastrophe

The spread of Xylella fastidiosa in Puglia — Italy's olive oil heartland — has destroyed millions of trees since 2013. Replanting with resistant cultivars (mainly Leccino and Favolosa) is underway, but olive trees take years to reach full production. The full recovery of Puglia's olive landscape is measured in decades, not seasons. For a region that produces nearly half of Italy's oil, this is an existential challenge.

The Cost Squeeze

Italian production costs are among the highest in the Mediterranean. Labour, energy, orchard management — everything has gone up, while the 2025/26 price correction has squeezed margins hard. Traditional, non-irrigated growers in the south are particularly exposed. When Tunisian EVOO costs half what Italian EVOO costs to produce, the competitive pressure is relentless.

Regulatory Muscle

On the positive side, Italy runs one of the world's tightest olive oil control systems. The SIAN digital traceability platform monitors stocks and bulk movements across the supply chain, and Italy has led EU efforts to crack down on fraud and mislabelling. For buyers concerned about authenticity, Italian-bottled oil comes with stronger traceability guarantees than most origins — though the system isn't perfect, and scandals still surface periodically.

What to Watch in 2026

The Italian olive oil market is at an inflection point. After two extraordinary years of tight supply and record prices, the return of more normal volumes is reshaping everything. Here's what matters:

Price direction: Italian EVOO will likely continue softening as 2025/26 supply is absorbed, but the premium over Spanish and Tunisian origin should hold. The key question is whether that premium narrows — and if it does, what it means for Italy's hub model margins.

Tunisia's quota battle: Any expansion of duty-free access would directly impact Italian blenders. This is one of the most politically charged issues in the sector right now, with Italian producer associations firmly opposed.

US tariff risk: The US is Italy's most valuable export market. EU olive oil faces tariffs of up to 15%, and any escalation would hit Italian bottlers hardest — they're the ones serving America's premium retail shelves.

Quality under pressure: The 2025/26 harvest was notably affected by olive fruit fly, degrading quality even where volumes were decent. Less DOP-eligible oil means tighter supply at the premium end, which could support high-end prices while bulk grades soften.

For anyone in the olive oil business, Italy remains the indispensable middleman — the country where production, trade, branding, and quality converge. Its dynamics don't just affect Italian oil; they ripple across the entire Mediterranean supply chain.

This analysis is part of OliveTerm's market intelligence coverage. For real-time olive oil prices, trade data, and market reports, access the OliveTerm Terminal.