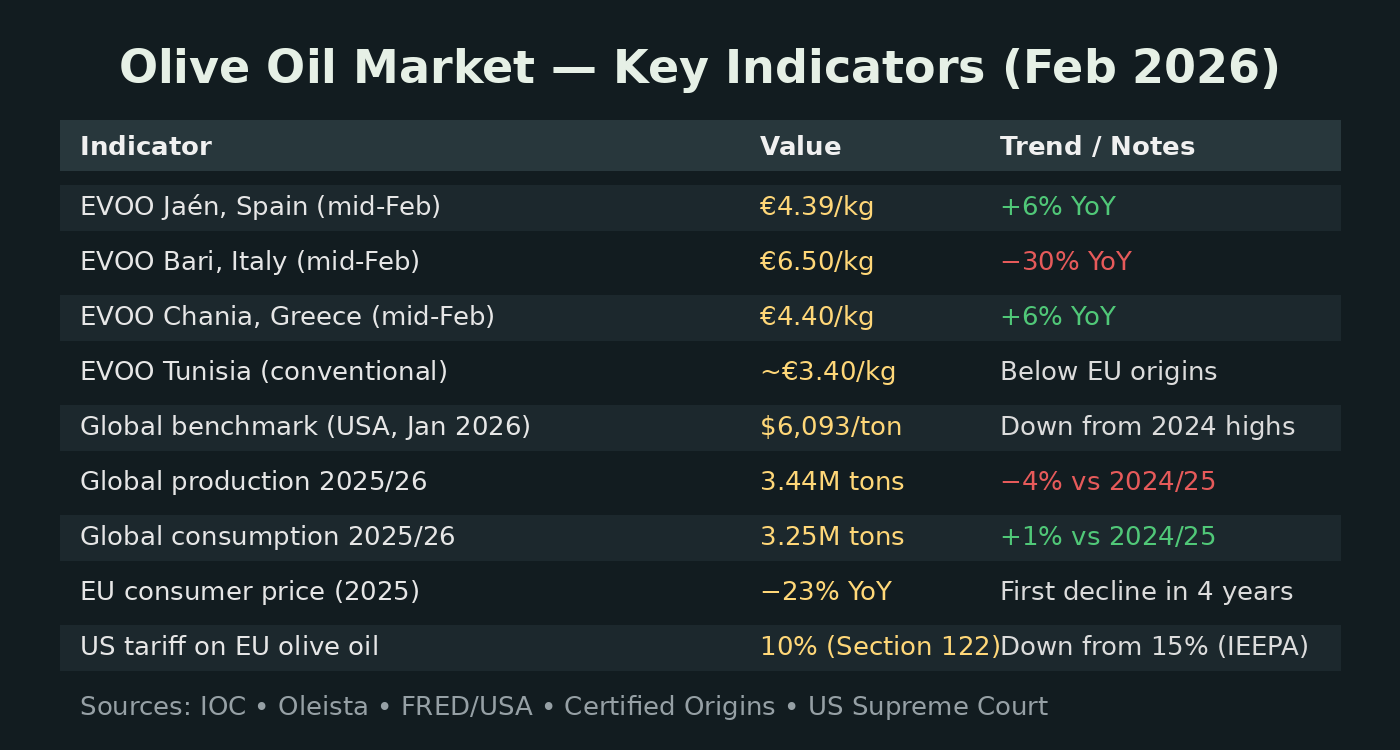

1. Executive Summary

The global olive oil market enters March 2026 navigating a complex transition. After the dramatic price spikes of 2023-2024 — driven by consecutive drought-affected harvests — origin prices have corrected sharply but remain above pre-crisis levels. The correction has been uneven across producing countries, creating significant price differentials that are reshaping trade flows and competitive dynamics globally.

In Spain, EVOO at origin climbed through February from EUR 407/100 kg in late January to EUR 439/100 kg by mid-February (+6% YoY), supported by lower-than-expected production after heavy December rainfall disrupted harvesting. In Italy, prices held at EUR 650/100 kg but are down 30% year-on-year thanks to a production recovery. Greece tracked Spain at EUR 440/100 kg (+6% YoY). Tunisia continues to undercut European origins significantly, with conventional EVOO at approximately EUR 3.40/kg.

Global production for the 2025/26 campaign is estimated at 3.44 million tons (-4% from 2024/25), still well above the crisis lows of 2023/24. Consumption is projected to reach 3.25 million tons (+1%), with the EU consumer price index for olive oil recording its first annual decline in four years (-23% in 2025). The most significant development in February was the US Supreme Court's ruling on the 20th striking down IEEPA-based tariffs as unconstitutional. President Trump immediately replaced them with a 10% global tariff under Section 122 of the Trade Act of 1974, effective for 150 days. For the olive oil sector, this means a shift from discriminatory 15% EU tariffs to a uniform 10% rate — a partial reprieve that levels the competitive playing field with non-EU producers.

2. Origin Prices by Country

Spain (Jaen)

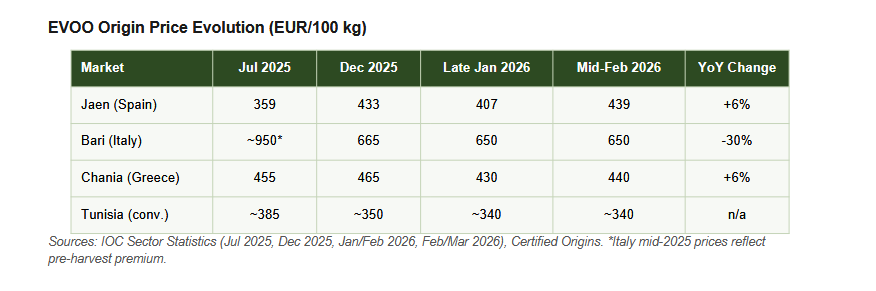

Spanish EVOO at origin climbed steadily through February 2026, rising from EUR 407/100 kg in late January to EUR 439/100 kg by the week of February 16-22 — a 6% increase compared to the same week of the previous campaign. Several factors drove this movement upward despite Spain's dominant global position. Cumulative production fell short of expectations. Heavy rainfall in November and December disrupted harvesting across Andalusia, reducing effective picking days by roughly two weeks. December output of 416,471 tons was 30% below December 2024. Cumulative production through December stood at approximately 716,372 tons, and total stocks of 715,735 tons were 24% below the prior year. In Jaen — the world's single largest olive oil region — persistent rain and limited labor availability contributed to an estimated 45% year-on-year decline, with some of the crop dropping to the ground as collection costs exceeded potential returns. On the demand side, both domestic and international buyers have increased purchases at these more attractive price levels. Conventional EVOO currently trades between EUR 4.50-5.00/kg, and certified organic at approximately EUR 5.50/kg. As of early March, the Oleista platform records an average Spanish origin price of EUR 4.50/kg.

Italy (Bari)

Italian EVOO at Bari held stable at EUR 650/100 kg through January and February 2026. This represents a steep 30% year-on-year decline, yet prices remain significantly above Spanish levels, reflecting Italy's structural premium driven by strong brand recognition and limited domestic supply. Production recovered to approximately 300,000 tons in 2025/26 (+30% from the previous campaign), led by strong output in Apulia and Calabria where timely summer rainfall offset spring drought effects. Despite the recovery, demand from large Italian bottlers — who source heavily from Spain, Tunisia, and Greece for blending — remains robust, supporting continued price differentiation.

Greece (Chania)

Greek EVOO at Chania was recorded at EUR 440/100 kg in mid-February (+6% YoY). Production is projected between 210,000 and 250,000 tons, a notable recovery from recent weak seasons. The Peloponnese is expected to contribute around 90,000 tons and Crete approximately 50,000 tons. Greek producers have been actively diversifying away from the US market following tariff uncertainty, redirecting exports toward Asia and the Middle East.

Tunisia & Turkey

Tunisia is the most aggressive price competitor in the global market. Conventional EVOO trades at approximately EUR 3.40/kg and organic at EUR 3.85/kg — substantially below all European origins. Tunisia has effectively replaced Italy as the world's second-largest producer by volume in recent campaigns and continues to push for greater duty-free access to the EU market. This price pressure is felt acutely across southern Europe, where Tunisian imports are displacing locally produced bulk oil in several markets. Turkey, after a record 505,000-ton campaign in 2024/25, is normalizing to an expected 150,000-170,000 tons — still significant for global balances.

Global Benchmark (USA)

The IMF global olive oil benchmark, published by the Federal Reserve Bank of St. Louis (FRED), stood at USD 6,092.93 per metric ton in January 2026. This represents a significant decline from the historic highs above USD 9,000/ton reached during the 2024 price crisis, confirming the normalization of global supply.

3. Consumer Price Dynamics

After rising 78% between 2022 and 2024, EU olive oil consumer prices declined 23% in 2025 — the first annual decrease after four consecutive years of increases. According to Eurostat data, the correction was most pronounced in the major producing countries where greater product availability transmits more quickly to retail shelves.

Among 35 European countries, Spain recorded the largest decline at 38.9%, followed by Greece at 29.2% and Portugal at 24%. These were the only three countries where prices fell by more than the EU average. Among the EU's four largest economies, France experienced the smallest decline, while Italy and Germany saw sharper drops. The EU Harmonised Index of Consumer Prices (HICP) for olive oil had already fallen 26% year-on-year by May 2025, with the deepest early declines recorded in France, Finland, and Romania.

Market analysts attribute the uneven correction to structural differences in the supply chain. As ASOLIVA director Rafael Pico has noted, in the main producing countries — Spain, Greece, and Portugal — the impact of a strong harvest is more direct and visible at both origin and consumer level. In importing countries, the pass-through is slower and dampened by packaging, transport, and retail margins. Alongside higher supply returning to average levels, weaker demand has contributed to pushing prices down. The sharp price increases of 2023-2024 triggered a significant shift toward cheaper alternative oils, and recovering those lost consumers requires sustained competitive pricing.

Looking ahead, consumer prices in 2026 are expected to stabilize around current levels, with only minor further corrections possible. The Portuguese Olive Oil Association (Casa do Azeite), which represents approximately 85% of branded packaged olive oil in Portugal, has projected no significant changes for 2026.

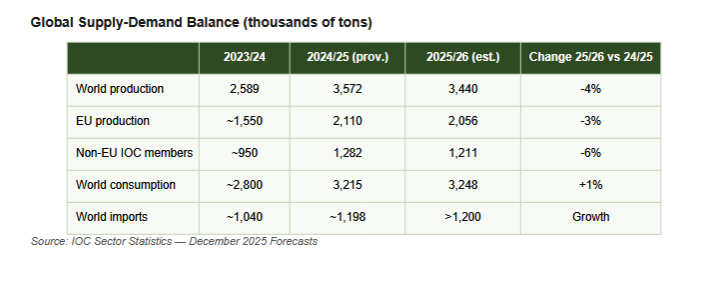

#4. Global Production — 2025/26 Campaign World olive oil production for the 2025/26 campaign is estimated by the IOC at approximately 3.44 million tons, a 4% decline from the strong 2024/25 rebound (3.57 million tons). Despite this contraction, output remains significantly above the crisis lows of 2023/24 (2.59 million tons) and above the five-year average of approximately 2.41 million tons for the six largest producing countries. The sector has clearly recovered from the supply shock, though the recovery is uneven.

IOC member countries are expected to produce 3.27 million tons (95% of global output). EU producers forecast 2.06 million tons (-3% vs the prior campaign), while non-EU IOC members project 1.21 million tons (-6%). World consumption is estimated at 3.25 million tons (+1%), and global imports and exports are expected to exceed 1.2 million tons each. On the EU demand side, consumption is projected at approximately 1.43 million tons, with exports of 765,000 tons and imports of 200,000 tons, suggesting a more stable balance after two highly volatile seasons.

5. Production by Country

5.1. Spain

Spain remains the dominant global producer, with 2025/26 output estimated between 1.37 and 1.44 million tons — approximately 3-8% below the previous campaign but 19% above the six-year average. Andalusia, responsible for roughly 70% of national output, produced around 1.08 million tons, penalized by a hot, dry autumn that reduced fruit size and oil content, particularly in rain-fed groves. The province of Jaen had to revise expectations down by about 20% due to drought and late-season rainfall disruptions. December production was 30% below the same month in 2024 after persistent rain halted harvesting for approximately two weeks. Regional variations are notable. Castilla-La Mancha, Spain's second-largest olive region with nearly 450,000 hectares, is holding output broadly steady at around 108,000 tons. Extremadura is seeing a slight increase to about 69,000 tons, driven by modern super-intensive plantations. Catalonia, however, continues to struggle with five consecutive years of drought, producing around 32,000 tons — well below historical averages.

5.2. Italy

Italy registered a clear production recovery in 2025/26, with output estimated at approximately 300,000 tons — up roughly 30% from the weak 2024/25 campaign. Apulia, which supplies more than half of Italy's olive oil, led the rebound alongside Calabria, both benefiting from timely summer rainfall that compensated for earlier spring dryness. Despite the recovery, Italy remains a net importer, relying heavily on Spanish, Tunisian, and Greek bulk oil for its large bottling and re-export industry.

5.3. Greece

Greek production is projected between 210,000 and 250,000 tons, improving on recent weak seasons. Early IOC estimates placed Greece at 250,000 tons (+30% YoY), while some analysts project closer to 210,000 tons (-15%). The Peloponnese, Crete, and other islands form the core producing regions. Greek olive oil continues to command a quality premium in several international markets, though the US tariff situation has prompted active diversification of export destinations.

5.4. Portugal

Portuguese production is estimated by the IOC at 177,000 tons (+10% YoY in its figures), though national forecasts from the INE project a productivity decline of approximately 20% due to adverse weather during flowering and significant olive grove destruction from 2024 summer wildfires. Other estimates range between 150,000 and 200,000 tons. Notably, Portuguese EVOO briefly traded below Spanish origin prices in January 2026, highlighting its role as a competitively-priced European origin.

5.5. Tunisia, Turkey & Other Origins

Tunisia remains a critical swing producer with a strong crop, aggressively positioning itself below European price levels. Tunisian stakeholders continue to push for expanded duty-free access to the EU beyond the current 100,000-ton quota. Turkey is normalizing after a record 505,000-ton campaign in 2024/25, with output expected between 150,000 and 170,000 tons — still meaningful for global supply dynamics. Morocco projects approximately 240,000 tons, up from a historical average of 160,000-180,000 tons.

6. Consumption & International Trade

6.1. Global Consumption Recovery

Global olive oil consumption exceeded 3.2 million tons in 2024/25 and is projected to reach 3.25 million tons in 2025/26 (+1%). The recovery is driven by the significant consumer price correction that has made olive oil accessible to households that had switched to cheaper vegetable oils during the 2023-2024 crisis. In Spain, retail purchases of EVOO had declined by 41% at the peak of the crisis — the most significant demand drop since the 1930s. The price normalization is reversing this trend, though the long-lasting effects of consumer switching in non-traditional markets remain a concern.

Import volumes in major markets increased 13.8% during October-December 2025 compared to the same period in 2024/25, with recovery observed across most markets except China and the United States. The EU unit value of extra-community olive oil exports fell to EUR 554/100 kg in May 2025 (-42.4% YoY), while volumes surged 36.1%, reflecting the classic post-crisis pattern of higher volume at lower value.

6.2. United States

US olive oil imports reached 437,309 tons in 2024/25 (+20.6% YoY). Spain, Italy, Tunisia, and Turkey jointly supply 88.6% of this volume, with virgin olive oils accounting for 73.5% of imports. Despite tariff headwinds, US consumption is forecast to reach a record high in 2025/26. However, early 2025/26 data (October-December 2025) shows a 1.6% decline in US purchases, while other major markets grew. This suggests tariff uncertainty is dampening procurement, with buyers limiting orders to immediate needs. The US remains structurally dependent on imports — domestic production in California covers approximately 5% of national consumption.

6.3. Brazil

Brazil accounts for 9% of global olive oil imports and 3.1% of world consumption. Although imports fell 11% in 2023/24 (to 81,000 tons) driven by high prices, the market has shown steady long-term growth. Portugal remains the primary supplier with 57% market share. The EU-Mercosur Partnership Agreement signed in January 2026 is expected to further strengthen this trade corridor by gradually reducing tariff barriers.

6.4. Emerging Market Channels

The tariff disruptions of 2025 accelerated market diversification. Throughout the year, many producing countries actively developed alternative channels in Asia and the Middle East. India represents significant long-term potential, with olive oil sales projected to reach EUR 198 million by 2028; a potential EU-India agreement would reduce Indian olive oil tariffs from 45% to 0% over five years. Egypt has also emerged as a major growth market for table olives and olive oil, with consumption rising from 11,000 tons in 1990/91 to 540,000 tons in 2024/25. Turkey and Algeria have similarly seen sharp domestic consumption increases.

7. US Tariff Developments

7.1. The Supreme Court Ruling (February 20, 2026)

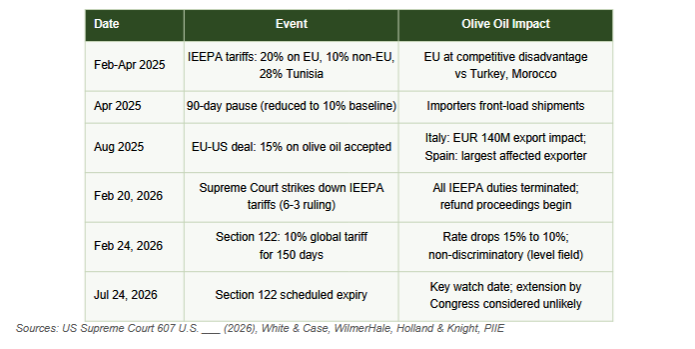

On February 20, the US Supreme Court held 6-3 in Learning Resources, Inc. v. Trump that the International Emergency Economic Powers Act (IEEPA) does not authorize the President to impose tariffs. Chief Justice Roberts, writing for the majority, concluded that IEEPA's grant of authority to "regulate importation" does not encompass the power to levy tariffs — a power constitutionally reserved for Congress. The Court emphasized that IEEPA contains no reference to tariffs, duties, or taxes, and that no previous president had ever interpreted the statute as conferring tariff authority. The majority applied the "major questions" doctrine, holding that delegation of such consequential economic power requires explicit congressional authorization.

All IEEPA-based tariffs were terminated as of February 24, 2026. This includes the 15% tariffs on EU olive oil and table olives that had been in effect since mid-2025. The Penn Wharton Budget Model estimates cumulative IEEPA tariff collections at approximately USD 165 billion, representing roughly half of all US customs duties collected over the period. Nearly 2,000 importers have filed refund cases in the US Court of International Trade, which has since ordered the refund of IEEPA duties and interest.

7.2. Section 122 Replacement

Hours after the Supreme Court ruling, President Trump issued a proclamation under Section 122 of the Trade Act of 1974 imposing a temporary 10% import surcharge on products from all countries, effective February 24. Section 122 authorizes tariffs of up to 15% for 150 days to address balance-of-payments deficits. The tariff is set to expire July 24, 2026, unless extended by Congress. The Peterson Institute (PIIE) has noted that the legal basis is questionable — the US does not have a balance-of-payments deficit in the technical sense, and the administration's own lawyers previously argued that Section 122 was no substitute for IEEPA authority.

7.3 Timeline

7.4. Sector Impact Assessment

The shift from 15% IEEPA tariffs to 10% Section 122 tariffs provides modest relief for European exporters. More importantly, the non-discriminatory nature of Section 122 eliminates the competitive distortion that previously favored Turkey and Morocco over EU producers. Spain, the largest olive oil exporter to the US with annual sales exceeding EUR 1 billion in 2024, stands to benefit most. The Spanish exporters' association (ASOLIVA) described the ruling as "very good news" for the sector. However, the broader market effects of the tariff episode persist. During the period of high US tariffs, olive oil normally destined for America was redirected within Europe, contributing to downward price pressure. Many EU producers simultaneously developed alternative export channels in Asia and the Middle East during 2025. If the Section 122 tariffs lapse in July without replacement, a rebound in US-bound exports could tighten EU supply and provide upward price support. Conversely, the administration may pivot to Section 301 or Section 232 investigations, which require findings of fact but could produce new tariffs within months.

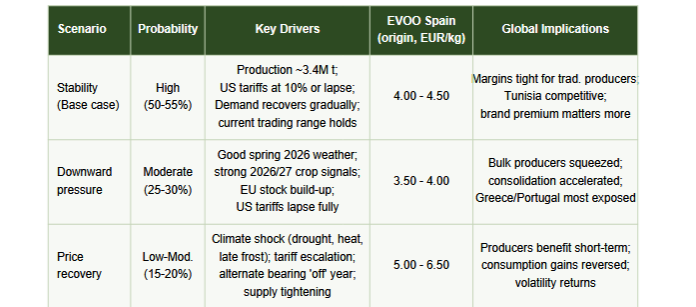

8. 2026 Outlook & Price Scenarios

The price trajectory for olive oil through the remainder of 2026 will be determined by the interplay of production fundamentals, the evolution of US tariff policy after the Section 122 tariffs expire in July, and the speed of demand recovery from the 2023-2024 price shock. Three scenarios are outlined below, weighted by probability.

8.1. Stability Scenario (Base Case)

Prices maintain the current EUR 4.00-4.50/kg range at Spanish origin through 2026. Spanish operators continue to defend this level as the minimum necessary for traditional groves to cover rising costs. EU consumption continues its gradual recovery, absorbing available supply without creating significant surpluses. The Section 122 tariffs either lapse in July or are replaced at a comparable 10-15% level, maintaining current trade patterns. This scenario favors branded and value-added producers who can capture the margin spread between bulk and retail pricing.

8.2. Downward Pressure Scenario

Favorable spring 2026 weather across the Mediterranean could set up a strong 2026/27 harvest expectation. Buyers anticipating a large crop would delay purchases, creating a buyer's market. Combined with continued Tunisian competition at EUR 3.40/kg and potential EU stock accumulation, Spanish origin prices could test the EUR 3.50-4.00/kg range. This scenario would be particularly challenging for producers in higher-cost regions who lack the scale economies of large Spanish or Tunisian operations.

8.3. Price Recovery Scenario

A significant climate event — extended drought in Andalusia, late frost in central Italy, heat wave during flowering — could materially reduce 2026/27 production expectations and trigger a price reversal. The natural alternate-bearing cycle also introduces risk: after a moderate 2025/26, the biological rhythm could produce either direction. Geopolitical escalation through Section 301 or Section 232 tariff authorities could also create regional price dislocations.

8.4. Structural Long-Term Growth

Beyond cyclical dynamics, the global olive oil market maintains a robust structural growth trajectory. Analysts project the market to grow from approximately USD 20.7 billion in 2025 to USD 31.7 billion by 2034 at a CAGR of 7.5%. Europe dominates with roughly 67% of revenue, while key growth drivers include expanding health awareness (cardiovascular benefits, antioxidant content), foodservice integration, and penetration into emerging markets. The competitive landscape is being reshaped by the rise of non-EU producers offering lower price points and by the shift toward super-intensive irrigated plantations.

8.5. Early Signals for Campaign 2026/27

Soil moisture conditions have improved following the heavy winter rainfall in the western Mediterranean. However, the critical period for the next harvest is the flowering window (April-June 2026), when temperatures, rainfall, and pest pressure will determine fruit set. Climate change continues to raise the baseline risk for olive production, with warmer temperatures, more frequent heat waves, and increasingly erratic rainfall creating new challenges for traditional rain-fed groves across the entire Mediterranean basin.

9. Strategic Recommendations

Inventory & sales timing: With the Section 122 tariffs set to expire July 24, producers and exporters should position inventory to capitalize on a potential rebound in US-bound demand. Avoiding bulk sales during the typical Q1 oversupply period and timing deliveries around tariff transition dates can protect margins.

Market diversification: The tariff episode has demonstrated the structural risk of over-reliance on any single export market. Proactively building positions in Brazil (EU-Mercosur agreement), India (potential EU-India deal with tariff reduction from 45% to 0%), East Asia, and the Middle East provides hedging against trade policy volatility. Brazil and India together represent some of the largest untapped growth potential globally.

Quality differentiation & branding: With Tunisian conventional EVOO at EUR 3.40/kg, competing on price is unsustainable for most European producers. Investment in PDO/PGI certification, early-harvest premiums, polyphenol content marketing, and organic certification provides essential margin protection. The growing consumer interest in traceability and origin authenticity supports premium positioning.

Direct-to-consumer channels: The price correction has re-engaged consumer interest in olive oil as an accessible premium product. Building brand equity through e-commerce, farm tourism, subscription models, and food experience platforms captures value that bulk commodity sales cannot. This is particularly relevant as a proposed US federal standard of identity for olive oil could improve quality transparency.

Climate resilience investment: Medium-term investment in irrigation infrastructure, drought-resistant cultivars, and grove management optimization is essential given the increasing frequency of adverse weather events. The shift toward super-intensive irrigated plantations offers higher yield security but raises water competition concerns in water-stressed Mediterranean regions.

Trade policy monitoring: Active monitoring of: (a) Section 122 expiry date and potential congressional extension; (b) Section 301 and Section 232 investigations that could produce new US tariffs; (c) Tunisian duty-free quota debate in Europe; (d) EU-Mercosur and EU-India implementation timelines; and (e) CIT refund proceedings which may influence importer purchasing patterns.

Disclaimer: This report is prepared using publicly available data from the International Olive Council (IOC), European Commission, Certified Origins, FRED/IMF, Oleista, Euronews, Olive Oil Times, Casa do Azeite, Agroportal, ASOLIVA, and other sector sources through March 12, 2026. Provisional figures may be subject to revision. This document does not constitute financial, commercial, or legal advice. Trade policy analysis reflects conditions as of March 12, 2026 and may change rapidly.